Global Market Commentary: First Quarter 2022

Markets Have Worst Quarter Since 1Q2020

Global equity markets had a volatile first quarter and when the final Wall Street bell rang on March 31st, global equity markets were in the red, as March was not enough to make up for the dismal returns from January and February.

But maybe the worst news was that the bond market suffered its worst quarter since 1980.

For the first quarter of 2022:

The DJIA ended Q1 with a loss of 5.2%;

The S&P 500 ended Q1 with a loss of 5.5%;

NASDAQ ended Q1 with a loss of 10.2%; and

The Russell 2000 ended Q1 with a loss of 8.9%.

The themes that drove market performance in the first quarter were the same themes that drove markets toward the end of last year. But in late February and throughout all of March, Wall Street dealt with the invasion of Ukraine by Russia and its impact on global markets.

Volatility and oil prices spiked this quarter, driven by a host of issues, including Russia’s invasion, rising inflation, supply chain issues and the Federal Reserve’s timing and size of rate hikes (we saw a 25 basis point hike in March).

The other themes were volatile consumer confidence, continued red-hot housing prices, high GDP growth numbers and corporate earnings that came in better than expected.

Further, we saw that:

Volatility, as measured by the VIX, trended up most of the month, more than doubling to a high of 36 on March 7th, before retreating to come to rest marginally higher than where it began the month.

West Texas Intermediate crude made a big move in the first quarter, starting at $75/barrel and ending the quarter at over $100. For perspective, WTI started 2021 at $48/barrel.

Market Performance Around the World

Investors were unhappy with the quarterly performance around the world, as 35 of the 36 developed markets tracked by MSCI were negative for the first quarter of 2022, with only MSCI Pacific ex-Japan advancing. And for the 40 developing markets tracked by MSCI, 26 of them were negative, with many posting staggering losses, including MSCI Eastern Europe that dropped almost 60%.

Source: MSCI. Past performance cannot guarantee future results

March Could Not Lift the Entire Quarter

U.S. equity markets reversed the negative course of the quarter’s first two months and ended March in positive territory. But it was still not enough to overcome the biggest two-month drop (January and February) since March 2020 as markets ended the 1st quarter of 2022 in the red - the first since the 1st quarter of 2020.

For the month of March:

The DJIA was up 4.2%;

The S&P 500 was up 5.2%;

NASDAQ was up 5.1%; and

The Russell 2000 was up 3.1%.

Sector Performance Rotated in Q12022

The overall trend for sector performance for all 3 months so far in 2022 was mixed and the performance leaders and laggards rotated throughout, giving investors a few mini sector rotations each month and during the quarter.

Here are the sector returns for the shorter time periods:

Source: FMR

Reviewing the sector returns for just the first quarter of 2022, we saw that:

9 of the 11 sectors were painted red for the first quarter, which is in stark comparison to the previous quarter;

The Energy sector turned in an astonishing quarter, driven by a massive jump in oil prices;

The defensive Utilities sector turned in a good quarter;

The interest-rate sensitive sectors (Information Technology and Financials specifically) struggled as the Fed raised rates by 25 bps; and

The differences between the best (+38%) performing and worst (-13%) performing sectors in the first quarter widened.

The Fed Increases Rates

The dominant theme this month (besides Russia/Ukraine) revolved around whether the Fed might need to raise short-term interest rates more quickly and more often, eating into future profits, especially within the high-flying tech names.

Then at the March meeting, the Federal Reserve moved its fed funds target rate from near zero to a range of 0.25% to 0.50%. It was the first rate hike since 2018.

The Federal Funds Rate – 10 Year Chart

But the Fed also released the so-called “dot plot,” which shows where individual Fed officials expect interest rates to be.

And given the surge in inflation numbers – from the perspectives of both consumers (CPI) and producers (PPI), the majority now expect seven hikes in 2022, four in 2023 and none for 2024. (In other words, there could be a rate hike at every remaining Fed meeting this year and at half the meetings next year.)

If this comes true, it would be higher than the Fed’s estimate of the long-run neutral rate, (which is 2%), and would suggest a more hawkish policy that could be more restrictive to growth.

Interestingly enough, when the Fed raised rates 25 basis points and released its “dot plot,” stocks rallied, suggesting that Wall Street appreciates the path that has been outlined.

But The Fed Was Not Unanimous

By its own metrics, however, it was becoming increasingly difficult for the Fed to forestall a rate increase at least in the range of 0.25%.

In fact, buried in a footnote of the Fed’s statement was this nugget:

“Voting against this action was James Bullard, who preferred at this meeting to raise the target range for the federal funds rate by 0.5 percentage points to 1/2 to 3/4 percent.”

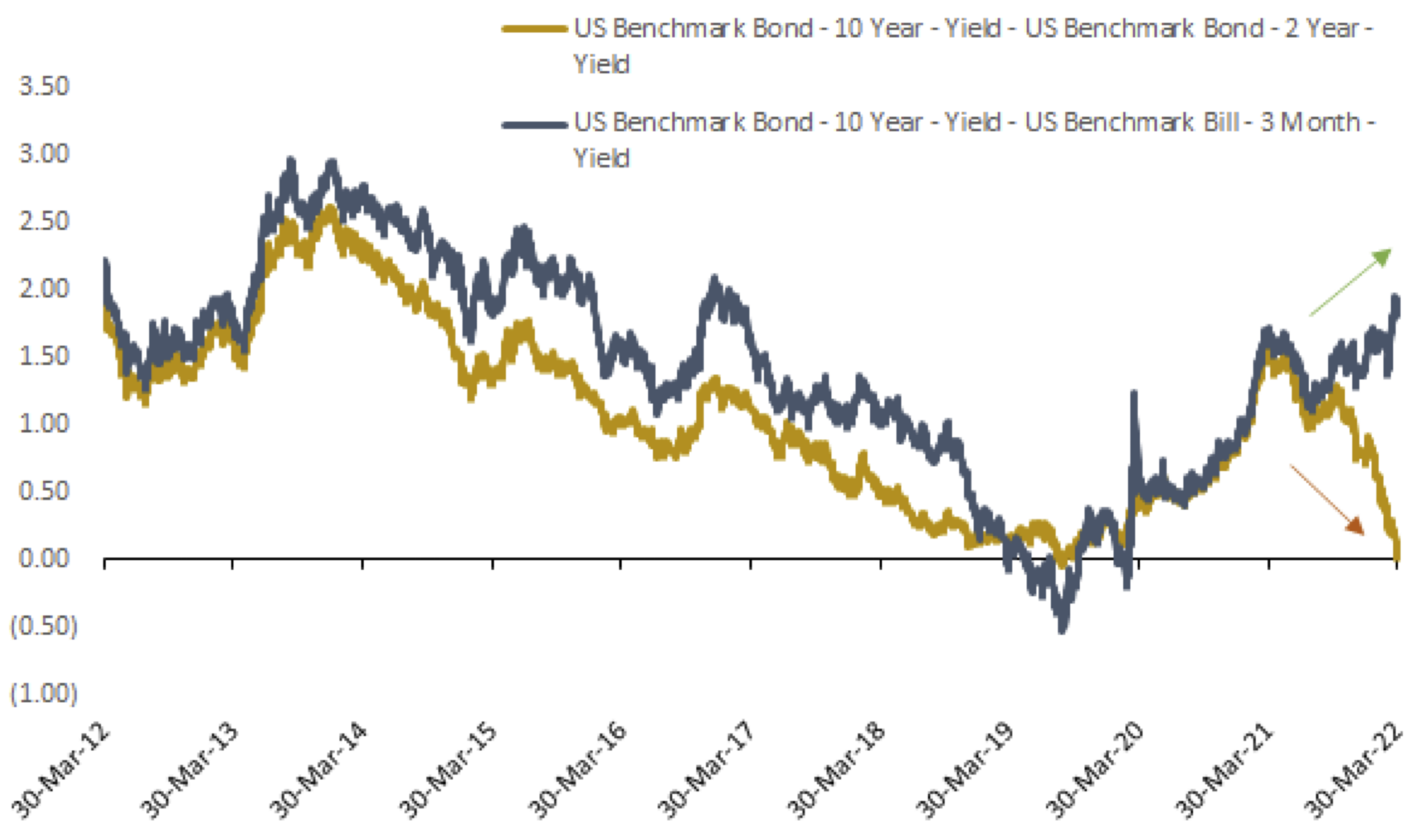

Bond Markets Struggle

At the end of the quarter, there was a lot of chatter because the 2-year Treasury yield and the 10-year Treasury yield inverted, leading many to suggest a recession is on the way in the next 12 months.

10YR-2YR Treasury curve and 10YR-3MTH Treasury curve (%)

But lost in much of the quarter-end summaries was this ominous sign: the bond market suffered its worst quarter since 1980. Specifically, the Bloomberg U.S. Aggregate Bond Index had its worst quarter since late 1980.

Want more bad bond news? Well,

The first quarter of 2022 was the third-worst quarter since the index’s inception.

March was the worst monthly performance for the index since July 2003.

GDP UP 6.9% Last Quarter

Two days before the quarter ended, the Bureau of Economic Analysis reported that real gross domestic product increased at an annual rate of 6.9% in the fourth quarter of 2021.

In the third quarter, real GDP increased 2.3 percent.

U.S. Bureau of Economic Analysis. Seasonally adjusted at annual rates.

PCE Price Index Up 6.4% Over 12 Months

The Bureau of Economic Analysis reported a lot of information on the last day of the quarter, including that:

Personal income increased $101.5 billion (0.5%) in February

Disposable personal income increased by $76.1 billion (0.4%)

Personal consumption expenditures increased $34.9 billion (0.2%)

Further:

Real DPI decreased 0.2% in February and Real PCE decreased 0.4%

Goods decreased 2.1%

Services increased 0.6%

The PCE price index increased 0.6%

Excluding food and energy, the PCE price index increased 0.4%

The PCE price index for February increased 6.4% from one year ago, reflecting increases in both goods and services.

Energy prices increased 25.7%

Food prices increased 8.0%

Excluding food and energy, the PCE price index for February increased 5.4% from one year ago

Personal Consumption Expenditures Price Index, Ex-Food and Energy

Change from Month One Year Ago

February 2022 5.4%

January 2022 5.2%

December 2021 4.9%

November 2021 4.7%

Unemployment is Very Low

Unemployment (3.8%) is now nearly at record lows. In addition, the number of job openings exceeds the number of unemployed by the widest margin in the past 20 years.

Record job openings exceed the number of unemployed (numbers in millions)

Source: FactSet

This paradigm suggests that we will be in a tight labor market for a while. And the jobs growth and unemployment numbers reported at the end of the quarter reinforce that notion.

Source: Bureau of Labor Statistics

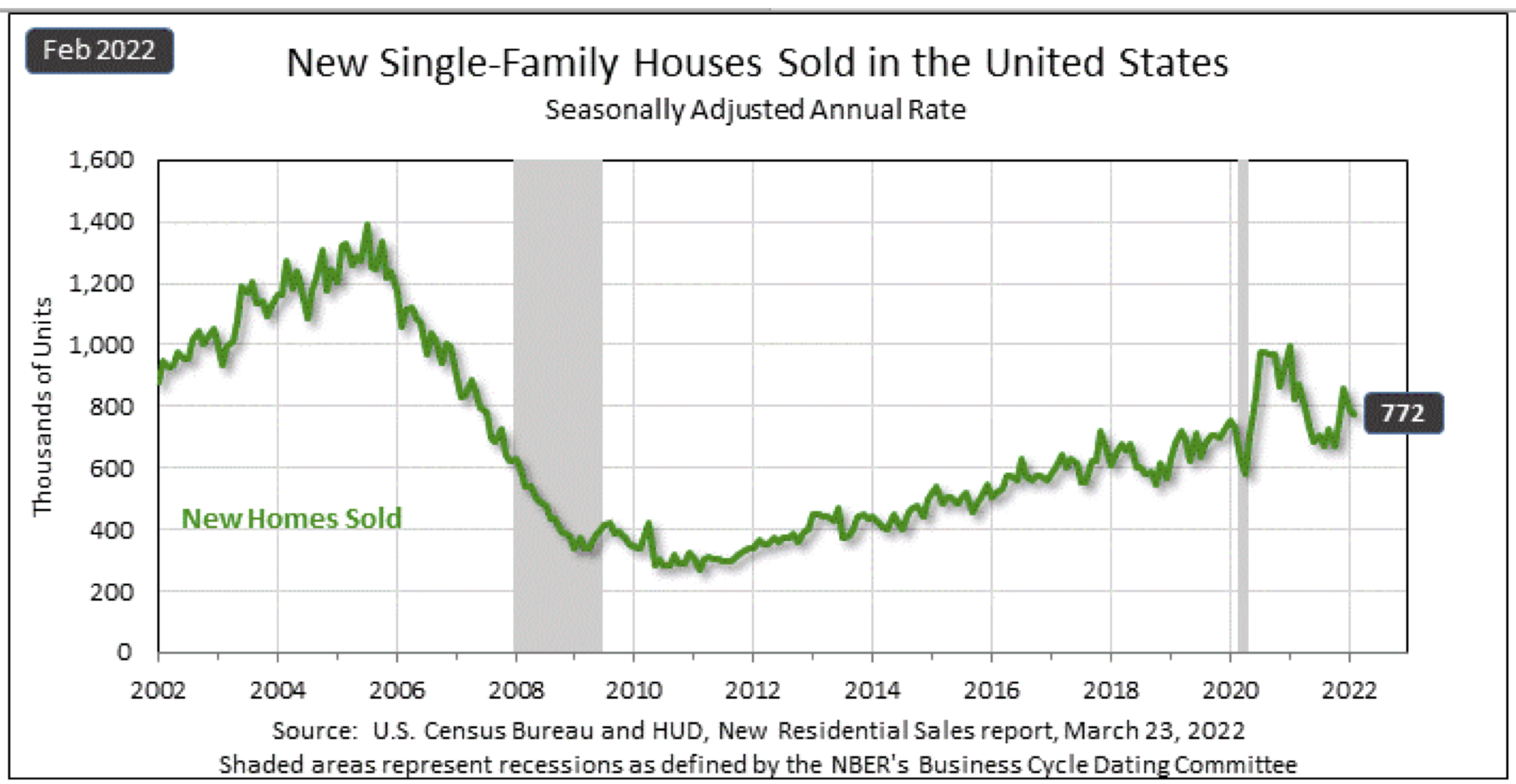

New Home Sales Down

The U.S. Census Bureau and the U.S. Department of Housing and Urban Development jointly announced the following new residential sales statistics for February 2022.

New Home Sales

Sales of new single‐family houses in February 2022 were at a seasonally adjusted annual rate of 772,000

This is 2.0% below the January rate of 788,000

This is 6.2% below the February 2021 estimate of 823,000

Sales Price, Inventory, and Months’ Supply

The median sales price of new houses sold in February 2022 was $400,600

The average sales price was $511,000

The seasonally‐adjusted estimate of new houses for sale at the end of February was 407,000

This represents a supply of 6.3 months at the current sales rate

Consumer Confidence is Up

The Conference Board announced that “the Consumer Confidence Index increased slightly in March, after a decrease in February. The Index now stands at 107.2 (1985=100), up from 105.7 in February. The Present Situation Index – based on consumers’ assessment of current business and labor market conditions—improved to 153.0 from 143.0 last month. However, the Expectations Index – based on consumers’ short-term outlook for income, business, and labor market conditions— declined to 76.6 from 80.8.”

Present Situation

Consumers’ appraisal of current business conditions improved in March.

19.6% of consumers said business conditions

were “good,” up from 17.6%.

22.1% of consumers said business conditions were “bad,” down from 25.1%.

Consumers’ assessment of the labor market also improved.

57.2% of consumers said jobs were “plentiful,” up from 53.5%, a new historical high.

9.8% of consumers said jobs are “hard to get,” down from 12.0%.

Expectations Six Months Hence

Consumers’ optimism about the short-term business conditions outlook declined in March.

18.7% of consumers expect business conditions will improve, down from 21.3%.

23.8% expect business conditions to worsen, up from 19.9%.

Consumers were mixed about the short-term labor market outlook.

17.4% of consumers expect more jobs to be available in the months ahead, down from 19.4%.

Conversely, 17.7% anticipate fewer jobs, down from 19.6%.

Consumers were also mixed about their short-term financial prospects.

14.9% of consumers expect their incomes to increase, up from 14.7%.

13.7% expect their incomes will decrease, up from 13.0%.

Sources: conference-board.org; bea.gov; census.gov; msci.com; fidelity.com; nasdaq.com; wsj.com; morningstar.com; bea.gov