For many medical professionals, the year begins with a sense of momentum.

Maybe you planned to save more, get more organized, reduce taxes, clean up old accounts, revisit your investments, or finally tackle a few financial decisions you have been putting off. January tends to bring that kind of energy. It feels like a fresh start.

Then real life takes over.

Work gets busy. Patient needs come first. Family schedules fill up. Administrative demands pile on. Tax season comes and goes. Before long, you are deep into the year and wondering where the time went.

That is exactly why a midyear financial check-in can be so valuable.

It is not because there is anything magical about the month of May. It is because this point in the year creates a natural opportunity to pause, step back, and evaluate whether your financial life is actually moving in the direction you want. By now, you have more than good intentions. You have real data. You have a better sense of your income, your spending, your savings habits, and the financial choices that may need your attention.

For nurse practitioners, anesthesiologists, pharmacists, dentists, veterinarians, and other medical professionals, this kind of review matters even more. Many people in healthcare are excellent earners, but their financial lives can still become more complicated than they need to be. A demanding career, high income, student debt, tax complexity, insurance needs, and limited time all create a unique set of challenges.

The good news is that a strong financial plan does not require constant attention. But it does require periodic attention.

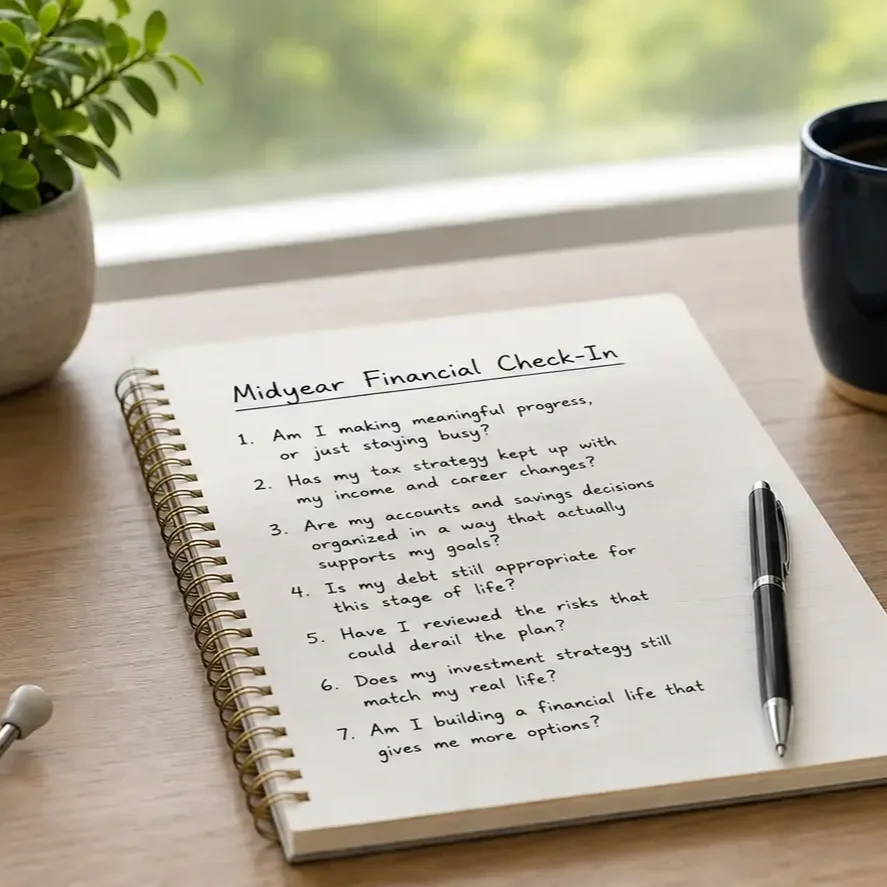

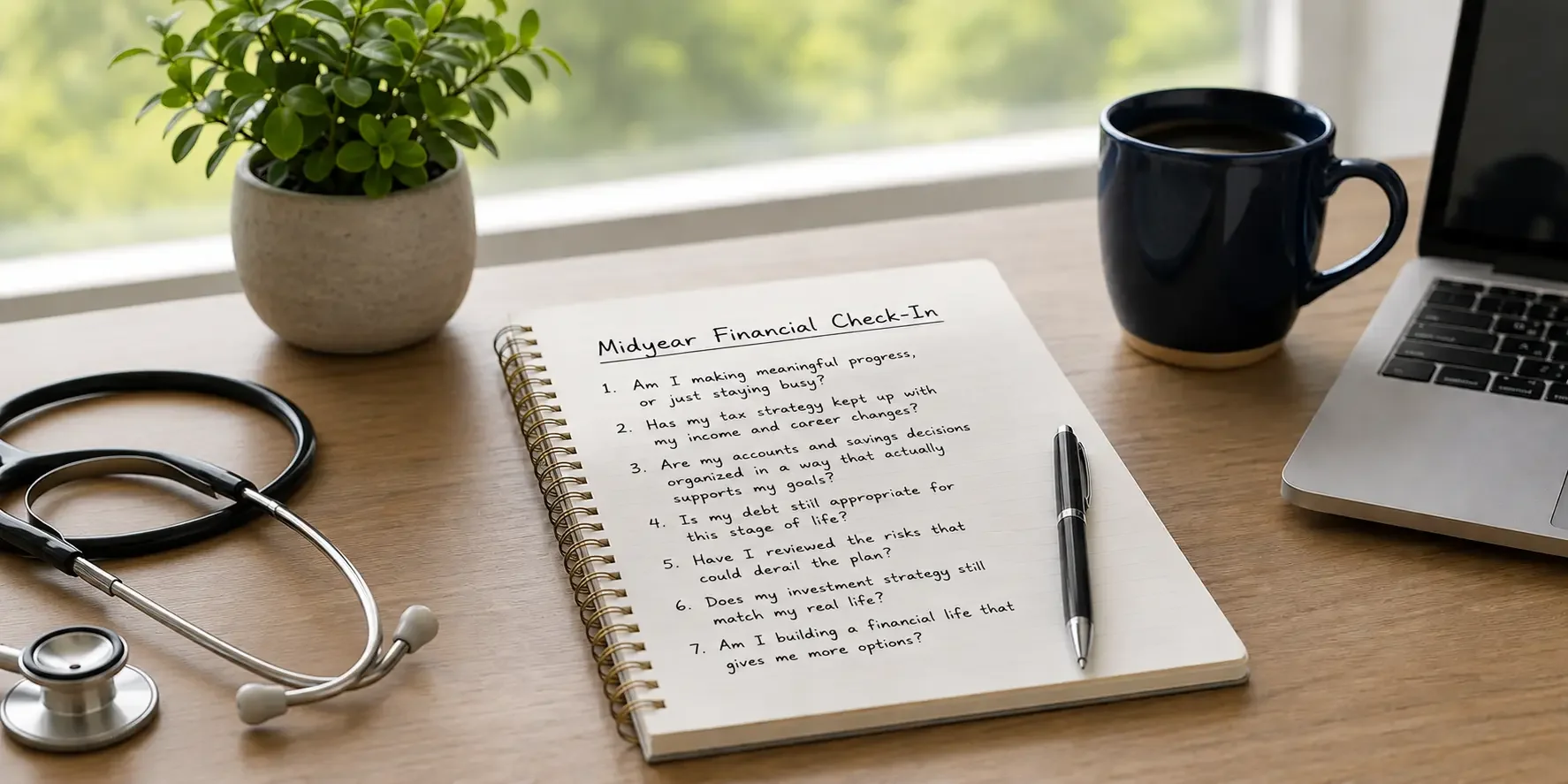

If you have not taken a close look at your finances since the beginning of the year, here are seven questions worth asking right now.

1. Am I making meaningful progress, or just staying busy?

This is often the best place to start because it gets to the heart of the issue.

Medical professionals are used to being productive. Your day is filled with responsibilities, decisions, and problems that need solving. You are constantly moving. That level of professional intensity can create a feeling that if you are working hard, things must be progressing everywhere else too.

But in personal finance, activity and progress are not always the same thing.

It is entirely possible to earn a great income, contribute to retirement accounts, pay down some debt, and still feel vaguely unsettled about where things are headed. That usually happens when financial decisions are being made in isolation instead of as part of a larger plan.

For example, maybe you are saving consistently but not really sure whether you are saving enough. Maybe you have increased your income but your cash flow somehow still feels tight. Maybe you have accumulated several accounts over the years and you know you should probably organize them, but it never becomes urgent enough to address.

A midyear check-in gives you the chance to ask a few honest questions:

Do I know how much I am saving this year?

Do I know what I am spending each month?

Have I improved my net worth, reduced financial stress, and/or increased flexibility?

Am I more organized than I was six months ago?

If I keep doing what I am doing now, where does that likely lead?

These are simple questions, but they can reveal a lot.

Sometimes the answer is reassuring. You may realize you are doing better than you thought. Other times, the answer highlights that you are operating on autopilot in areas that deserve more intention.

Neither outcome is bad. The goal is clarity.

A financial plan does not have to be perfect to be effective. But it should make it easier to understand whether your efforts are actually moving you closer to your goals.

2. Has my tax strategy kept up with my income and career changes?

For high-income earners, tax planning is rarely something that should be addressed only once a year.

That is especially true for medical professionals, because income often changes in ways that are not fully reflected in an old withholding setup or a once-a-year conversation with a tax preparer. A raise, a bonus, production-based compensation, moonlighting income, self-employment income, partnership income, or a spouse’s career change can all shift the tax picture in meaningful ways.

When those changes happen but the tax strategy stays the same, small problems can become expensive ones.

By the middle of the year, you usually have a much clearer picture of what this year may look like. That makes it a good time to review whether your current tax approach still makes sense.

Here are a few areas worth reviewing:

Withholding and estimated payments

If your income is variable or higher than expected, your withholding may no longer be sufficient. On the other hand, some people significantly overwithhold and create unnecessary cash flow pressure during the year. Neither situation is ideal.

A midyear review can help you decide whether adjustments are needed before the problem gets larger.

Retirement plan contributions

Are you on track to maximize available employer plans? If you have access to a 401(k), 403(b), 457(b), SEP IRA, solo 401(k), cash balance plan, or another tax-advantaged account, this is a good time to assess whether those opportunities are being fully used.

For high earners, account selection and contribution timing can matter more than people realize.

Roth versus pre-tax decisions

For some households, the better decision may be to reduce current taxes through pre-tax contributions. For others, especially those earlier in their peak earning years or expecting future tax increases, building Roth assets may deserve more attention.

The right answer depends on the broader context, not just this year’s deduction.

Charitable giving and other tax-sensitive planning

If charitable giving is part of your financial life, there may be smarter ways to structure it. The same goes for capital gains planning, donor-advised funds, bunching deductions, or timing certain income and expenses.

The point is not to make tax planning overly complicated. The point is to be proactive while there is still time to act.

Tax planning works best when it supports your broader goals, improves efficiency, and reduces unpleasant surprises. Midyear is a good time to make sure your strategy is doing all three.

Learn more about tax strategy in our previous blog, You Filed Your Taxes - Now What? 7 Smart Moves Every Medical Professional Should Make

3. Are my accounts and savings decisions organized in a way that actually supports my goals?

Many medical professionals are saving diligently, but not always with a system that is easy to understand or maintain.

Over time, it is common to build up a collection of accounts:

current employer retirement plans

old 401(k) or 403(b) accounts

Roth IRAs

taxable brokerage accounts

HSAs

emergency savings

529 plans

joint accounts

business accounts

checking and savings accounts with different banks

None of that is inherently problematic. In fact, it often reflects years of responsible behavior. But it can also create fragmentation.

When your financial life becomes scattered across too many places, it is harder to answer basic planning questions:

Which money is for retirement?

Which money is for shorter-term goals?

Which accounts offer the most flexibility?

Which assets are most tax-efficient to spend later?

Am I taking more investment risk in one account than I realize?

Are there old accounts that should be consolidated or revisited?

Disorganization does not always show up as a crisis. Often it shows up as background friction. You feel like you should understand your finances better than you do. You know money is being saved, but the structure feels messy. You are not sure whether each account still serves a clear purpose.

That kind of friction matters because complexity tends to discourage action.

When your accounts are organized well, decision-making becomes easier. You can invest more intentionally, evaluate your progress more clearly, and reduce the mental clutter that often comes with managing a high-income household.

This can also be a good time to review beneficiary designations, account titling, and whether your investment allocation still reflects your time horizon and actual goals.

Sometimes a midyear review does not require dramatic changes. Sometimes it is just a matter of simplifying what is already there.

4. Is my debt still appropriate for this stage of life?

Debt is one of the most common financial realities for medical professionals, and one of the most misunderstood.

There is a tendency to treat debt in extremes. Some people believe all debt is bad and should be eliminated as fast as possible. Others assume that as long as the interest rate is manageable, there is no reason to think about it much at all.

In reality, debt needs context.

Student loans, mortgages, practice loans, business lines of credit, and even car loans may all be part of a reasonable financial picture. The real question is whether the debt still fits your current stage of life, your income, your goals, and your stress tolerance.

Midyear is a good time to ask:

Has my income increased enough that I should accelerate payoff?

Am I carrying any high-interest debt that deserves immediate attention?

Am I comfortable with the tradeoff between investing and paying down debt?

Is my current debt load limiting flexibility more than I want?

If interest rates stay higher for longer, does my plan still work?

For younger professionals, carrying some debt while focusing on career growth and systematic saving may be perfectly sensible. For others, especially those getting closer to retirement or simply wanting more peace of mind, reducing liabilities may become a much higher priority.

The right answer depends on your circumstances. But one thing is usually true: debt should be managed intentionally, not passively.

If you have not revisited your repayment strategy in a while, now may be a good time to do it.

Learn more about a practical framework to evaluate your debt in one of our previous blogs, How Much Debt Is Too Much? A Simple Framework for Medical Professionals to Stay Financially Fit

5. Have I reviewed the risks that could derail the plan?

A financial plan is not just about accumulating assets. It is also about protecting what you are building.

This is an area where many medical professionals know what they should do, but often delay. The topics are not especially fun, and they do not usually feel urgent. But that does not make them less important.

A midyear check-in is a good time to review the risks that could disrupt your plan if left unaddressed.

That may include:

disability insurance

life insurance

umbrella liability coverage

health insurance options

emergency reserves

estate documents

powers of attorney

beneficiary designations

For medical professionals in particular, disability coverage deserves close attention. Your ability to earn an income is often your greatest financial asset, especially in the earlier and middle phases of your career. If that income were interrupted, the impact could be significant.

At the same time, as assets grow, liability exposure may increase as well. Umbrella coverage is often overlooked, even in households with substantial earnings and savings.

Estate documents are another area that tends to get postponed. Many people assume estate planning is something to address later in life. In reality, once you have a spouse, children, assets, or responsibilities that would fall on others, it becomes relevant much sooner.

You do not need to obsess over every possible risk. But you do want reasonable protection around the things that matter most.

A good financial plan is not just designed to work when everything goes right. It is also designed to remain resilient when life becomes more complicated than expected.

6. Does my investment strategy still match my real life?

Investment allocation should not be based only on what sounds reasonable in theory. It should be based on your actual life.

That includes your time horizon, your need for growth, your need for stability, your tolerance for market declines, your career stage, your upcoming spending needs, and the role your portfolio is supposed to play.

This is where many people get tripped up.

A portfolio may have been set up years ago and left largely untouched. Or changes may have been made in response to market headlines rather than as part of a disciplined process. In other cases, the risk level may look acceptable on paper, but feel very different when markets become volatile.

That is why midyear can be a good time to revisit a few core questions:

Why is my portfolio allocated the way it is?

How much risk am I actually taking?

Would I stay invested if markets fell sharply?

Am I holding enough cash for near-term needs?

Does my portfolio reflect my goals, or just generic rules of thumb?

Risk tolerance and risk capacity are not the same thing.

You may feel comfortable with market risk emotionally, but not have the cash flow or time horizon to absorb major declines at the wrong time. Or you may have strong financial capacity but still lose sleep over volatility.

A good investment plan should reflect both.

It should also connect to the rest of your financial life. Investment strategy works best when it is coordinated with taxes, retirement timing, spending needs, and broader planning priorities.

If your portfolio has not been reviewed recently, or if it no longer feels connected to your actual goals, this is a good time to revisit it.

7. Am I building a financial life that gives me more options?

This may be the most important question of all.

For many medical professionals, financial success is not just about reaching a specific net worth number. It is about creating options.

Options to work less. Options to retire on your own terms. Options to change roles, start a practice, take a sabbatical, help family, or simply feel less dependent on the next paycheck.

That kind of flexibility rarely comes from one big decision. It usually comes from a series of smaller decisions made consistently over time.

You build options by:

saving systematically

keeping lifestyle creep in check

managing debt thoughtfully

using tax-efficient strategies

protecting against major risks

investing with a purpose

organizing your financial life so it is easier to manage

In other words, you build options by planning.

A midyear review is not about perfection. It is about making sure your money is helping create a life with more freedom, not just more complexity.

If that is happening, great. Keep going.

If it is not, that is useful to know too. There is still plenty of time this year to make meaningful adjustments.

Final Thoughts

Medical professionals spend their careers helping others make thoughtful decisions under pressure. But when it comes to personal finance, even very smart and successful people can end up reacting instead of planning.

That is why a midyear check-in can be so helpful.

It creates a moment to pause and ask whether your income, savings, taxes, debt, investments, and protection strategies are all working together in a way that supports your goals. It helps you move from good intentions to real alignment. And it gives you a chance to make course corrections before small issues become bigger ones.

You do not need a perfect plan. You do need a current one.

If your financial life feels more complicated than it should, or if you simply want a clearer sense of where you stand, this can be a great time to take a fresh look.

Need a second opinion?

If you are a medical professional and want help reviewing your financial plan, tax strategy, retirement trajectory, or overall financial organization, I would be glad to help you think it through.

At Outside The Box Financial Planning, I help medical professionals make smarter financial decisions so they can protect their nest egg, reduce tax liability, and move toward retirement with more confidence and clarity.

If you want help evaluating your retirement income plan, tax strategy, and investment positioning, you can schedule an Introductory "Fit" Meeting.